A banking service is sometimes thought a complex and sophisticated activity in many countries and it is also widely confused with a banking product or a banking operation. However, a banking service is quite different in meaning and yet is still being explored what actually it is. The greatest advantage of the banking service is often regarded as having a distance service quality and it is more attractive and incomparable objective than other financial institutions. Not to mention the fact that, a banking service is today measured by reliability, convenience and again quality.

A large part of the operations previously executed by the banking representatives are now made by the calculation systems, and thus, they deal with the problem of the optimum usage of these systems in order to obtain maximum performance with the lowest possible cost. At the banking level there is ferocious competence to get the best and most attractive product, the largest number of clients, the largest number of branches and banking ATMs, the best trained personnel, and competence sharpens senses and directs attention to innovative and profitable solutions. At the same time with the intensification of this competence, banks will largely invest in the efficiency and solution development that can differentiate them on the market.

Distance banking deeply transformed the way of communicating, distribution, marketing and sales regarding the banking operations. Thus, communication is made indirectly or with the help of some people that are not visible or perceivable for the consumer. In what distribution is regarded, distance banking adds a supplementary channel to the existing one, permits a fine segmentation of products, and banking specialists consider that next to the classic products, clients could buy a new one.

After analyzing the capacity of increasing the distance banking services made by the banking marketers, the following things were observed:

– a consumer out of three never goes to the bank unit and therefore he cannot be considered a target consumer;

– the interviewed consumers considered that distance banks represent the most adequate interface for current operations;

– although clients are faithful to the traditional agency, one cannot exclude in the future to try new methods that could allow them a much more comfortable approach of services;

– the rapid growth of internet users leads to the promotion of distance banking;

– the dynamization of the account number is exponential, so we assist to the democratization of banks by making them closer to the population.

Distance banking services present a major impact upon banking companies and clients having advantages on both sides. Each bank client must go to a bank unit at certain periods of time, hardly facing the urban traffic and the front-office queues. But with distance banking services, clients can operate their transactions from their office, from home or anywhere else with the help ofan Internet connection. Studies indicate that, between 9–11 a.m, 22–23 % of the total volume of online visits is made by those who access the banking sites. The second peak is between 5–7 p.m when 13–14 % of the total connections at the end of the day and after the closing of banking agencies. The permanent access to their accounts, mainly atthe time of the front-office opening, which are still constraining especially for those who work, comfort, discretion and time gaining constitute real advantages for the clients.

The users of these services may be divided in two categories:

– „the practitioners”, are those active people who do not have too much time for banking operations and they use a distance banking service to simplify their life;

– „the modernists”, characterized by a high level of mobility, the fans of high-tech, that are not interested in the human side of the client-bank counselor relationship.

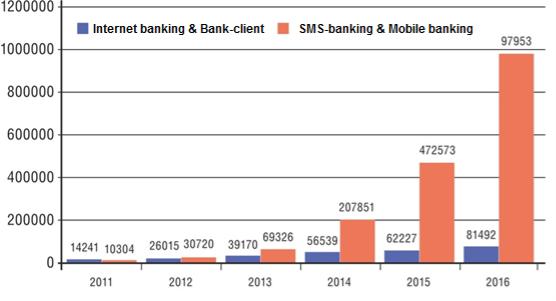

Fig. 1. The number of users of distance banking services according to their types [2]

With reference to the recent statistic information, as of 1st January 2016, the number of users of distance banking services in Uzbekistan is soaring year by year. As it is clearly seen in the column graph the number of SMS-banking and mobile banking services accounted for 979530 units and internet banking and bank-client 814920 units of the mentioned period. In comparison with 1 January 2015, the number of users of SMS banking and mobile banking rose nearly double times and internet banking and bank — client units rose by 19265..

Up to a point, distance banking services are more prevalent everywhere and banks are apparent to broaden their activities through them, what is more, to the best of our knowledge, these services are a key point to appeal constant clients for a long-term, but an effective mutual partnership.

The difficult economic period we are going through has had a boost of eBanking services, leading to a more careful both banks to promote their clients how to understand the benefits of banking transactions in front of the computer. The need to reduce costs has led banks to transfer partof operations to the greatest possible alternative channels, which provide lower costs.

On the other hand, customers are more aware of the price paid for banking services, the time spent on speed and security operations. The conclusion is simple: the benefits from such services worldwide!

All things considered, as I have said, distance banking services are the most successive power of commercial banks and they may be superseded by no other services in case they bring more profit and detain clients for long time with their comfort in modem economic society.

References:

- Modern Banking. Shelagh Heffernan, Professor of Banking and Finance, Cass Business School, City University, London.

- www.cbu.uz The website of The Central bank of the Republic of Uzbekistan

- Bank of England (1984b), ‘‘The Business of Financial Supervision’’,Bank of England Quarterly Bulletin.