The article discusses the theoretical aspects of personnel accounting for remuneration. The basic concept and essence of reward is given. Messages related to payroll are presented.

Keywords: Salary, wages, accounting, payroll calculations.

Remuneration of labor is one of the main factors of the social and economic life of each country, collective, and individual. It is the main source of income for the overwhelming number of workers, which means that it represents a powerful incentive to increase labor productivity and productivity. Labor accounting is one of the most time-consuming and responsible accountants.

The relevance of the topic is that remuneration is a complex part of the functioning of any commercial organization, since it is remuneration that brings income to the family budget.

Salary is a remuneration for labor depending on the qualifications of the employee, the complexity, quantity, quality and conditions of the work performed, as well as compensation payments (surcharges and allowances of a compensatory nature, including for work in conditions that deviate from normal, work in special climatic conditions and territories affected by radioactive contamination, and other payments of a compensatory nature) and incentive payments (surcharges and allowances of a stimulating nature, bonuses and other incentive payments).

Remuneration of labor is a system of relations related to ensuring the establishment and implementation by the employer of payments to employees for their labor.

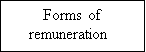

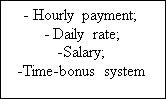

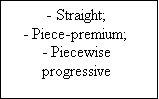

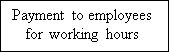

There are several forms of remuneration. The main forms of remuneration are time and piecework. Forms of remuneration are presented in figure 1.

![]()

![]()

![]()

![]()

Fig. 1. Forms of remuneration

There are two types of wages — primary and secondary (Figure 2).

![]()

![]()

![]()

![]()

![]()

![]()

![]()

![]()

![]()

![]()

![]()

![]()

![]()

![]()

![]()

![]()

![]()

Fig. 2. Types of wages

The normative regulation of accounting for settlements with payroll personnel is presented by the following documents: Federal Law «On Accounting”, the Labor Code of the Russian Federation, the Tax Code of the Russian Federation, Regulation on Accounting and Financial Reporting in the Russian Federation, as well as other regulatory documents.

In organizations, to summarize information on settlements with personnel for pay, account 70 «Settlements with personnel for pay» is intended. Table 1 shows the main accounting entries for account 70 «Settlements with staff for remuneration».

Table 1

Accounting records for accounting of calculations with personnel for remuneration

|

The fact of economic life |

Debit |

Credit |

|

Accrued wages to employees |

20,23,25,26 |

70 |

|

Benefits from social insurance funds were accrued |

69.1 |

70 |

|

Benefits accrued from the organization |

20,23,25,26 |

70 |

|

Withholding tax on personal income |

70 |

68 |

|

Salary paid from the cash register |

70 |

50 |

|

Deposited wages |

70 |

76.4 |

|

Accrued wages due to the reserve for vacation pay |

96 |

70 |

Various deductions and deductions are made from the amounts of payroll. Deductions are divided into three groups: mandatory, on the initiative of the employer, at the request of the employee.

Analytical accounting of remuneration in organizations is carried out using personal accounts. Personal accounts are opened for each employee upon employment.

So, the main tasks of labor accounting and its payment are:

– accounting of the employee’s personnel, the time worked by them on the volume of work performed;

– the correct calculation of the amounts of payment and deductions;

– accounting for settlements with employees of the organization, the budget and extrabudgetary funds;

– the correct allocation of accrued wages and deductions to social needs.

Settlements with staff on wages is one of the most important and responsible areas of accounting in any organization.

The payroll accountant must be a qualified professional. He should regularly monitor changes in legislation — amendments to regulations, deductions rates for the PFR, FSS, FFOMS, vacation and sick leave payments, benefits for dismissal.

References:

- Labor Code of the Russian Federation. Part Three of December 30, 2001 No. 197 — Federal Law (as amended on April 1, 2019)

- Federal Law of December 6, 2011 No. 402-ФЗ «On Accounting» (as amended on November 28, 2018)

- Khoruzhiy L. I. and other Accounting financial accounting. — Publishing House — MTAA 2012.

- Khoruzhiy L. I. Management accounting in agriculture: a textbook for students of agricultural Universities — Moscow: Publishing House of the RSAU-MTAA, 2012.

- Transformation of tax legislation in the digital economy/L. I. Khoruzhy, D. I. Ryakhovsky, V. I. Khoruzhy, K. A. Dzhikiya, D. D. Postnikova//Research Journal of Pharmaceutical, Biological and Chemical Sciences. 2019. Т. 10. № 1. С. 2000–2003

- Modern problems of accounting, economic analysis and statistics / L. I. Khoruzhiy, A. I. Pavlychev, E. I. Stepanenko, V. I. Khoruzhiy abd others. — M., 2017.

- Khoruzhiy L. I., Accounting And Economics: Modern Methodology And Development Trends / Kharcheva I. V., Postnikova D. D., Postnikova L. V., Ostapchuk T. V., Korzhavina T.Yu., Urazbakhtina L. V., Kerimov V. E., Makhmudov A. R., Pavlychev A. I., Evgrafova L. V., Livanova R. V., Makunina I. V., Chutcheva Yu.V., Khoruzhiy L. I., Akaeva A. S. //. Moscow, 2018.